The Demand Side of the Trades Crisis

Written by Santosh Sankar, 2026-04-21

Every reshoring announcement assumes the workforce exists to execute it. Every new factory coming online assumes the welders to build it and the millwrights to maintain it are there. Every industrial expansion assumes pipefitters are available to run the systems that keep it operating.

None of these assumptions are true.

The skilled trades shortage is not a single problem. It is three separate demand explosions hitting the same labor pool simultaneously, on top of a retirement wave that was already pulling experienced workers out faster than new ones could replace them. Understand each curve individually and you understate the problem. The convergence is what makes this structural.

Reshoring Wants Workers it Can't Find

In the Reshoring Initiative's 2025 survey of 500 US manufacturers, workforce availability ranked above tariffs, tax cuts, and deregulation as the single biggest barrier to bringing production back to the US.

Companies are telling policymakers directly: the incentives are improving, the economics are moving in our direction, and we still can't commit because the people don't exist. Even without a reshoring surge, 2.1M manufacturing jobs are forecast to go unfilled by 2030, with an estimated $1T GDP cost attached to that gap.

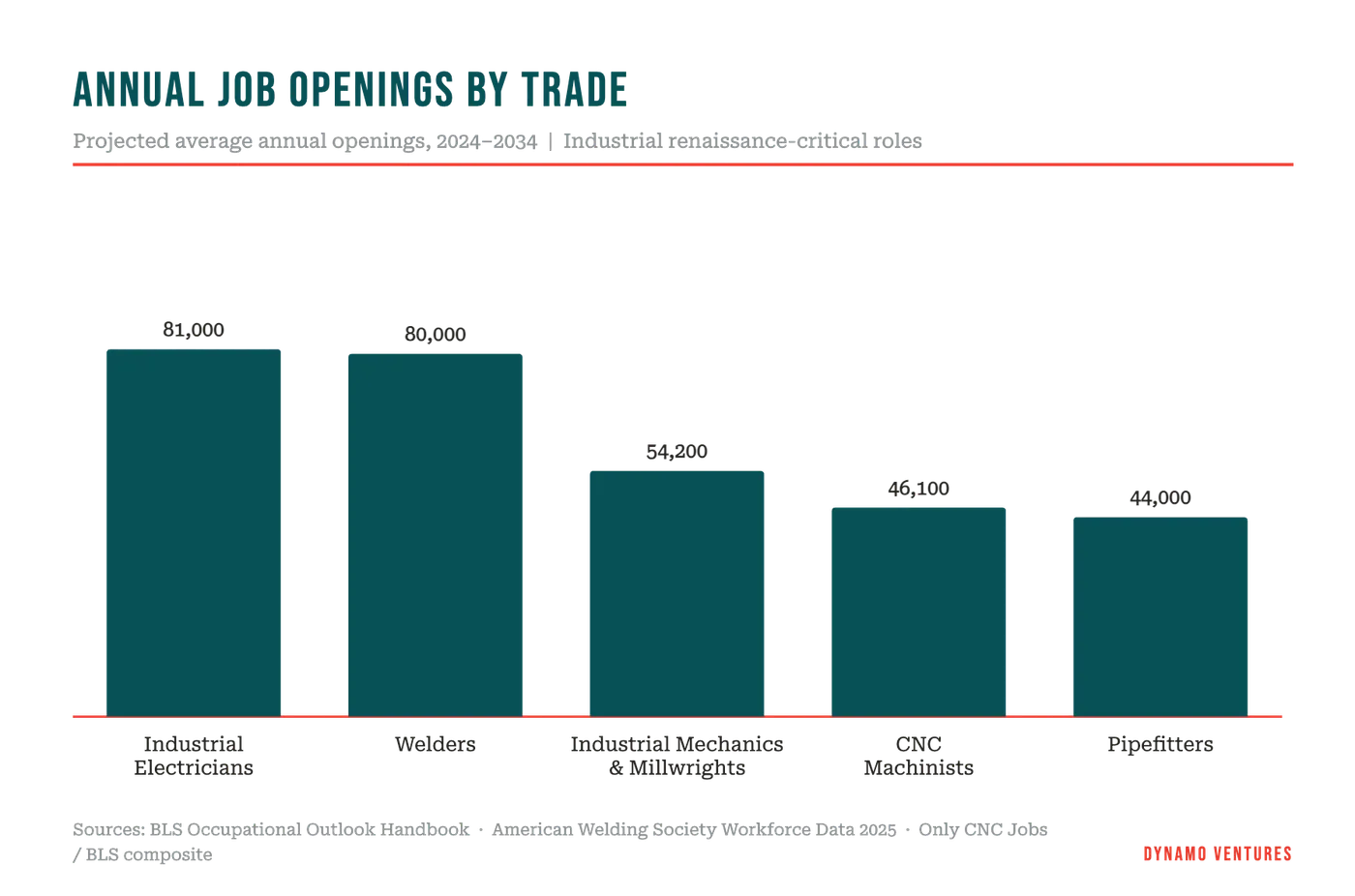

The Five Trades the Industrial Economy Runs On

The roles the industrial renaissance actually depends on are specific. Five stand out. Not because they're the only trades that matter, but because the gap between supply and demand in each is severe, the tie to reshoring and industrial buildout is direct, and the training path is defined enough to build a pipeline around.

Welders. Every factory, refinery, and pipeline depends on welded joints. The American Welding Society projects 80k welding openings annually through 2029, against a projected shortage of 330k to 360k welders by 2027. The average age of a US welder is 55. For every five retiring, two are entering the field. Welding also has the shortest credentialing path of any role on this list: 6 to 12 months to a deployable welder, and the broadest placement surface. Every sector here needs them.

Pipefitters. Industrial facilities run on pressurized piping systems moving gases, fluids, and steam through manufacturing plants, chemical facilities, and refineries. The BLS projects 44k openings per year through 2034, driven overwhelmingly by replacement demand as experienced pipefitters age out. These are not residential plumbers. Industrial pipefitters require years of apprenticeship and specialized certification for high-pressure systems. That timeline cannot be compressed on demand, which makes early pipeline investment the only lever available.

Industrial Mechanics and Millwrights. When a factory goes down, a millwright gets it back up. These are the workers who install, align, maintain, and repair the machinery inside every industrial facility. The BLS projects 54.2k openings per year through 2034, with the occupation growing at 13%, fastest of any role on this list. Reshoring doesn't just need someone to build the factory. It needs someone to keep it running on day two, and every day after.

Industrial Electricians. Not the same as a commercial electrician. Factory floor work involves control systems, programmable logic controllers, automated equipment, and high-voltage industrial wiring. A distinct skill set with distinct certifications. Every reshored facility needs industrial electricians before it can produce a single unit. The broader electrician shortage is well documented: 81k openings annually, with the workforce projected to shrink 14% by 2030 as demand grows 25%. The industrial subset of that shortage is the least trained-for and most acutely felt on the factory floor.

CNC Machinists. The sleeper on this list. Every advanced manufacturing facility runs on CNC, computer numerical control machines that produce precision parts for aerospace, defense, medical devices, automotive, and energy. The BLS projects roughly 46k CNC-related openings annually through 2034, almost entirely replacement demand as the current workforce, median age over 50, retires out. The training path is 18 to 24 months for a deployable operator, longer for multi-axis programmers. Employers across aerospace and defense report CNC scarcity as a direct constraint on production capacity. Most trade schools don't train for it at all.

Together these five trades represent roughly 225k annual openings, the majority of them replacement demand. The pipeline filling those seats is a fraction of what's needed.

The Demand Curves Compounding the Shortage

Each of these trades was already under pressure before the current reindustrialization cycle began. Three forces are now landing simultaneously.

Manufacturing reshoring is accelerating. 245k manufacturing jobs were announced in 2024. Each new domestic facility requires welders to construct it, pipefitters to run its systems, millwrights and industrial electricians to maintain its equipment, and CNC machinists to operate its production lines. The workforce to staff those functions doesn't scale with the announcement calendar.

Infrastructure spending is peaking. The IIJA committed $550B in new spending, with peak labor demand arriving now through 2027. Roads, bridges, water systems, refineries, and industrial facilities all draw on the same trades pool. That spending doesn't create workers. It competes for the ones that exist.

Compute infrastructure has become an industrial competency. This is the least understood demand vector. Meta, Microsoft, Amazon, Google, and Oracle committed a combined $700B in capital expenditure in 2026, much of it flowing into data centers. Building and operating these facilities is not a software problem. It requires the same trades as a manufacturing plant. Welders fabricate the structural steel. Pipefitters design and install the cooling systems that keep high-density compute racks from overheating. Industrial electricians commission the high-voltage power infrastructure. Over 400 data centers are currently under development across the US, competing directly with reshoring projects for the same pipefitters, the same welders, and the same industrial electricians. Sander van't Noordende, CEO of Randstad, put it plainly: the real constraint on global tech growth isn't a shortage of chips, energy, or capital. It's the scarcity of specialized talent to build the physical infrastructure. BlackRock put $100M behind that observation to fund trades workforce training. Capital is starting to recognize what industrial operators have known for years.

The Retirement Wave is the Accelerant

40% of the current construction and industrial workforce is expected to retire by 2031. Policy levers pulled today, apprenticeship programs, curriculum investments, federal workforce initiatives, will not produce journeymen before 2028 or 2029 at the earliest. The pipeline and the demand curve are not on the same timeline.

That gap doesn't close through a business cycle. It closes through institutional infrastructure that doesn't currently exist at the scale required. The trades workforce was systematically deprioritized for forty years. Funding cut. Cultural prestige stripped. Employer-to-institution pipelines severed. The industrial economy was then rebuilt on the assumption those workers would appear when needed.

They won't.

What makes this moment distinct is that the physical infrastructure of AI and the physical infrastructure of American manufacturing are now drawing from the same depleted labor pool. The shortage isn't additive. It's compounding. The bottleneck to the industrial renaissance is not capital, policy, or technology. It is people with specific, non-codifiable skills that took years to develop and decades to accumulate. That is where durable companies get built.

This piece is the first in Dynamo's physical economy series on the trades workforce. The next piece details what the trade school of the future needs to look like and where we see the investment opportunity.